Geral

Editorial do WSJ

Federal spending will hit a new record this year

With the recovery sputtering, the White House and its allies have been blaming government spending cuts, or what the neo-Keynesians call "fiscal contraction." This is a dubious economic theory even if spending were being cut, but yesterday's mid-year report from the Congressional Budget Office shows definitively that there's been nothing close to contraction in Washington.

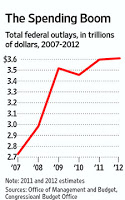

That's the real news in the CBO numbers, which show that spending in fiscal 2011 (which ends on September 30) will hit a new high of $3.6 trillion, up $141 billion from 2010. That's higher than the previous record in 2009 of $3.5 trillion, which was supposed to be the peak of the "temporary" stimulus spending.

As the nearby chart shows, that is also nearly $900 billion more spending than in 2007. Total federal outlays will have increased by roughly one third in a mere four years. This hasn't happened since the Great Inflation of the late 1970s.

Give President Obama and the two Pelosi Congresses credit for this much: They said they would spend our way out of recession, and they sure gave it the old Beltway try. The problem is that we got the spending without the promised economic growth.

This is the real cause of our current deficit and debt woes. As a share of the economy, spending will once again come in at nearly 23.8%, up from 20.7% as recently as 2008. Defense spending is expected to increase by only $14 billion to $703 billion in 2011, despite the surge in Afghanistan. The bigger increases are in Medicare, Medicaid, and the usual panoply of entitlements and other payments to individuals.

All of this means the deficit will roll in at nearly $1.3 trillion, or 8.5% of GDP this year. That's down a mere $10 billion from fiscal 2010, and we suppose taxpayers should be grateful for small fiscal favors.

The reason for this small deficit dip is that total tax revenues will climb in fiscal 2011 by about $150 billion. Individual income tax receipts will increase this year by about 21%, or $190 billion, though tax rates have stayed the same. Even with this good news, revenues will still come in at only 15.3% of GDP, which is far below the modern historical average of more than 18%.

Revenues would have been about $115 billion higher without the temporary payroll tax cut pressed by President Obama. But that tax cut hasn't provided any economic lift, and overall growth simply isn't fast enough to get revenues back to normal. Merely returning to an average economic expansion would reduce the deficit by 3% of GDP a year, or hundreds of billions of dollars.

Looking forward, CBO forecasts a sunnier fiscal picture, but it is based on assumptions that will never come true. The deficit is projected to fall to $973 billion in fiscal 2012, then fall again to $510 billion in 2013, and to a mere $265 billion in 2014.

But this assumes that federal spending will grow by only $12 billion in 2012, a level of spending control that even Ronald Reagan never achieved. President Obama wants much more spending next year and so does the Senate. Oh, and Medicare payments to doctors will fall by nearly 30% starting in 2012. Congress has been promising this cut in payments since 1997, but it never happens and would hurt medical care if it did.

The rest of CBO's fantasy forecast comes from what it says will be "the sharp increases in revenues that will occur when provisions of [the Bush era tax cuts extended last year] expire." So CBO estimates that federal taxes as a share of GDP will leap to 19% in 2013 and 20.2% in 2014 from 15.3% today. And we are supposed to believe that economic growth will soar to 4.4% and 5% in 2014 and 2015 after huge tax increases on capital gains, dividends, small businesses and workers in 2013. Beam us up, Scotty.

With these optimistic assumptions, CBO is able to forecast that federal debt held by the public will rise only to a peak of 73% in 2013 before falling to 67% in 2016. We think economist David Malpass is closer to the truth when he predicts a debt to GDP ratio closer to 85% in 2016 and 100% in 2021 without significant reform.

The real story told by the CBO report is that the federal government is still pursuing a very loose fiscal policy, despite lamentations from Democrats and the Keynesian economists who populate Wall Street. The best that House Republicans have been able to do so far is to battle Mr. Obama and Senate Democrats to a draw, delaying tax increases until 2013 and preventing even larger spending increases. To really control Washington's appetites, the voters are going to have to back up their message in 2010 with reinforcements in 2012.

- The Amazing Obama Budget

Editorial do WSJ Federal budgets are by definition political documents, but even by that standard yesterday's White House proposal for fiscal year 2013 is a brilliant bit of misdirection. With the abracadabra of a tax increase on the wealthy and...

- The 2013 Tax Cliff

Editorial do WSJ President Obama unveiled part two of his American Jobs Act on Monday, and it turns out to be another permanent increase in taxes to pay for more spending and another temporary tax cut. No surprise there. What might surprise Americans,...

- The Latest Jobs Plan

Editorial do WSJ If President Obama's economic policies have had a signature flaw, it is the conceit that by pulling this or that policy lever, by spending more on this program or cutting that tax for a year, Washington can manipulate the $15 trillion...

- America Gets Downgraded

Editorial do WSJ Whatever one thinks of the credit-rating agencies—and we aren't admirers—it serves no good purpose to shoot the fiscal messengers. Friday's downgrade by Standard & Poor's of U.S. long-term debt to AA+ from AAA will be...

- The Obama Downgrade

Editorial do WSJ So the credit-rating agencies that helped to create the financial crisis that led to a deep recession are now warning that the U.S. could lose the AAA rating it has had since 1917. As painfully ironic as this is, there's no benefit...

Geral

What Austerity?

Editorial do WSJ

Federal spending will hit a new record this year

With the recovery sputtering, the White House and its allies have been blaming government spending cuts, or what the neo-Keynesians call "fiscal contraction." This is a dubious economic theory even if spending were being cut, but yesterday's mid-year report from the Congressional Budget Office shows definitively that there's been nothing close to contraction in Washington.

That's the real news in the CBO numbers, which show that spending in fiscal 2011 (which ends on September 30) will hit a new high of $3.6 trillion, up $141 billion from 2010. That's higher than the previous record in 2009 of $3.5 trillion, which was supposed to be the peak of the "temporary" stimulus spending.

As the nearby chart shows, that is also nearly $900 billion more spending than in 2007. Total federal outlays will have increased by roughly one third in a mere four years. This hasn't happened since the Great Inflation of the late 1970s.

Give President Obama and the two Pelosi Congresses credit for this much: They said they would spend our way out of recession, and they sure gave it the old Beltway try. The problem is that we got the spending without the promised economic growth.

This is the real cause of our current deficit and debt woes. As a share of the economy, spending will once again come in at nearly 23.8%, up from 20.7% as recently as 2008. Defense spending is expected to increase by only $14 billion to $703 billion in 2011, despite the surge in Afghanistan. The bigger increases are in Medicare, Medicaid, and the usual panoply of entitlements and other payments to individuals.

All of this means the deficit will roll in at nearly $1.3 trillion, or 8.5% of GDP this year. That's down a mere $10 billion from fiscal 2010, and we suppose taxpayers should be grateful for small fiscal favors.

The reason for this small deficit dip is that total tax revenues will climb in fiscal 2011 by about $150 billion. Individual income tax receipts will increase this year by about 21%, or $190 billion, though tax rates have stayed the same. Even with this good news, revenues will still come in at only 15.3% of GDP, which is far below the modern historical average of more than 18%.

Revenues would have been about $115 billion higher without the temporary payroll tax cut pressed by President Obama. But that tax cut hasn't provided any economic lift, and overall growth simply isn't fast enough to get revenues back to normal. Merely returning to an average economic expansion would reduce the deficit by 3% of GDP a year, or hundreds of billions of dollars.

Looking forward, CBO forecasts a sunnier fiscal picture, but it is based on assumptions that will never come true. The deficit is projected to fall to $973 billion in fiscal 2012, then fall again to $510 billion in 2013, and to a mere $265 billion in 2014.

But this assumes that federal spending will grow by only $12 billion in 2012, a level of spending control that even Ronald Reagan never achieved. President Obama wants much more spending next year and so does the Senate. Oh, and Medicare payments to doctors will fall by nearly 30% starting in 2012. Congress has been promising this cut in payments since 1997, but it never happens and would hurt medical care if it did.

The rest of CBO's fantasy forecast comes from what it says will be "the sharp increases in revenues that will occur when provisions of [the Bush era tax cuts extended last year] expire." So CBO estimates that federal taxes as a share of GDP will leap to 19% in 2013 and 20.2% in 2014 from 15.3% today. And we are supposed to believe that economic growth will soar to 4.4% and 5% in 2014 and 2015 after huge tax increases on capital gains, dividends, small businesses and workers in 2013. Beam us up, Scotty.

With these optimistic assumptions, CBO is able to forecast that federal debt held by the public will rise only to a peak of 73% in 2013 before falling to 67% in 2016. We think economist David Malpass is closer to the truth when he predicts a debt to GDP ratio closer to 85% in 2016 and 100% in 2021 without significant reform.

The real story told by the CBO report is that the federal government is still pursuing a very loose fiscal policy, despite lamentations from Democrats and the Keynesian economists who populate Wall Street. The best that House Republicans have been able to do so far is to battle Mr. Obama and Senate Democrats to a draw, delaying tax increases until 2013 and preventing even larger spending increases. To really control Washington's appetites, the voters are going to have to back up their message in 2010 with reinforcements in 2012.

- The Amazing Obama Budget

Editorial do WSJ Federal budgets are by definition political documents, but even by that standard yesterday's White House proposal for fiscal year 2013 is a brilliant bit of misdirection. With the abracadabra of a tax increase on the wealthy and...

- The 2013 Tax Cliff

Editorial do WSJ President Obama unveiled part two of his American Jobs Act on Monday, and it turns out to be another permanent increase in taxes to pay for more spending and another temporary tax cut. No surprise there. What might surprise Americans,...

- The Latest Jobs Plan

Editorial do WSJ If President Obama's economic policies have had a signature flaw, it is the conceit that by pulling this or that policy lever, by spending more on this program or cutting that tax for a year, Washington can manipulate the $15 trillion...

- America Gets Downgraded

Editorial do WSJ Whatever one thinks of the credit-rating agencies—and we aren't admirers—it serves no good purpose to shoot the fiscal messengers. Friday's downgrade by Standard & Poor's of U.S. long-term debt to AA+ from AAA will be...

- The Obama Downgrade

Editorial do WSJ So the credit-rating agencies that helped to create the financial crisis that led to a deep recession are now warning that the U.S. could lose the AAA rating it has had since 1917. As painfully ironic as this is, there's no benefit...